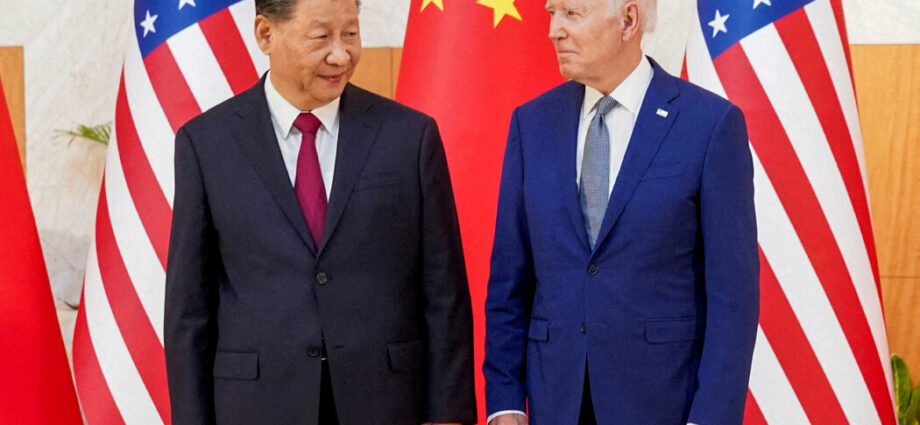

Doing business in China is getting even harder

The Biden administration is expected to announce new restrictions today on investing in China, its latest effort to prevent Beijing from accessing advanced technologies that could be used by its military.

The new measures add to the challenges facing the world’s second-largest economy as it faces a post-pandemic slowdown. But they also highlight the growing difficulties for and global companies operating in China, a day after a major Western law firm said it would leave the country.

The rules will focus on high-tech sectors. Biden’s executive order will bar private equity and venture capital firms from investing in Chinese industries including quantum computing, artificial intelligence and advanced semiconductors, people familiar with the deliberations told the Times.

China’s economy is already being squeezed. Official data released today showed the country had fallen into deflation last month, a day after Beijing reported that trade had plummeted by the most since the start of the pandemic.

Businesses that bet big on China are caught in the middle. Dentons, the largest Western law firm in China in terms of staff, said yesterday it would separate from Dacheng, its unit there. The two firms merged in 2015, and Dentons even added Chinese characters to its logo to signal its commitment to the country.

China’s new counterespionage law has made operating there more difficult. It banned the transfer of any information related to national security — but did not define which data would fall under this rubric. The law also allowed authorities to access data, electronic devices and personal property, as well as to block individuals from leaving the country.

That made it impossible to follow legal industry standards and best practice, a person familiar with Dentons’ decision-making told DealBook. For example, a provision that requires Chinese firms to keep the names of clients and employees secret from foreign entities raised thorny issues for American lawyers, who must check for conflicts with existing clients before taking on a new one.

These problems are widespread across industries. “Standards are diverging between China and Western economies,” Eswar Prasad, a trade policy professor at Cornell and a former head of the I.M.F.’s China division, told DealBook. “It’s all driven by the phenomenon that China is not as open to foreign business as it once professed to be.”

Chinese authorities have raided the offices of Western-linked consulting firms in recent months, and the venture capital firm Sequoia broke off its unit in the country in June. Employees at financial firms operating in China have reportedly been forced to attend lessons in the ideology of President Xi Jinping.

But the Chinese market may still be too big to ignore. Keyu Jin, an economist and the author of “The New China Playbook,” said companies operating there have always had to balance competing needs. “Consumer companies have big dreams in China,” she told DealBook. “Foreign financial institutions eye significant returns on the trillions of household wealth that needs to be managed.”

China is a major economy and foreign businesses will continue to work there, Prasad added, even if it’s becoming “quite a fraught proposition.”

HERE’S WHAT’S HAPPENING

A warning from Moody’s drags down bank stocks. The credit ratings agency put shares of six major lenders on watch for a potential downgrade, and cut the ratings of several regional banks, citing lower income and higher funding costs tied to rising interest rates. Shares in firms like Bank of New York Mellon and Cullen/Frost Bankers fell as much as 2.8 percent.

Regulators fine financial companies $549 million over misuse of messaging apps. Eleven institutions, including Wells Fargo and BNP Paribas, were accused by the S.E.C. and the Commodities Futures Trading Commission of failing to police employees’ use of “off-channel” services like WhatsApp for business communications. Wall Street banks had already paid $1.8 billion in fines for similar violations last year.

WeWork raises questions about its future. The beleaguered co-working company said in a regulatory filing that it faces “substantial doubt” about its ability to continue as a going concern, the starkest sign yet that it may collapse. WeWork shares, which were already trading for pennies, fell more than 16 percent after market hours on the news.

ESPN gets into the sports-betting business. The Disney-owned sports network struck a 10-year deal with Penn Gaming, which will operate an online sports book and pay ESPN $1.5 billion for access to its brand, marketing and talent for promotional purposes. The transaction will replace the sports book’s previous brand, Barstool Sportsbook, with ESPN Bet; relatedly, Penn will sell Barstool Media back to its founder, Dave Portnoy.

Chipotle’s founder raises money for his second act

Thirty years ago, Steve Ells opened the first Chipotle in Denver and went on to build a $51 billion fast-casual dining giant. Now he is working on his next act: a quick-serve, plant-based restaurant concept that relies on automation.

That start-up, Kernel, has raised $36 million in Series A financing, DealBook’s Michael de la Merced is first to report. That will help the company open its first location in New York City this fall — and develop technology it can eventually license to others.

How Kernel works: It’s a hub-and-spoke model, with a central kitchen that does much of the prep work throughout the day. The food is then biked to restaurants; there, machines and a small crew of humans assemble everything for customers.

The restaurant will offer an array of plant-based dishes, including a crispy faux-chicken sandwich, a veggie burger and a chicken Caesar salad without, well, chicken. (The focus on plants is meant to be eco-friendly, though Ells concedes that it was hard to create dishes that appealed broadly.)

Kernel builds on lessons Ells learned from Chipotle. When he began the start-up after leaving Chipotle three years ago, he focused on improving efficiency, speed and food quality through software and automation.

The result, Ells said, is a chain that can operate smaller restaurants in more locations (since they don’t need bulky kitchen equipment) and be more consistent in meal quality. It also needs fewer employees, but Ells said that Kernel will be able to pay them more.

The fund-raising effort came after two years of self-financing by Ells. He secured investments from groups including Raga Capital, Willoughby Capital and Rethink Food.

What next? Kernel will open its first restaurant this fall, and has ambitions to operate 15 locations within two years.

Eventually it could license its technology to other chains. “There’s no question that more and more automation is going to make its way into restaurants,” Ells said. Of Kernel, he added, “Once the hard work is done, once the platform is proven, it’s very, very simple to replicate.”

How media giants are trying to stay on top of A.I.

As the corporate world reckons with the disruption posed by artificial intelligence, some media giants are reportedly working on ways to marshal the fast-evolving technology — even as many of the artists they work with remain skeptical.

Universal Music is in talks with Google over licensing “deepfake” work, according to The Financial Times. If successful, that could lead to tools that would allow consumers to use imitations of singers’ voices and melodies in new work, paying owners for the right to do so. (Artists could choose to opt in.)

Universal Music has been worried about tech companies exploiting works by its artists — who include Drake and Taylor Swift — without compensation. And Google is hoping that new A.I. tools will keep it competitive with the likes of Microsoft.

Meanwhile, Disney has created an A.I. task force, according to Reuters. The group is meant to figure out how to deploy the technology across the Disney empire, from its movie and TV studios to its ad business. The company has almost a dozen job listings seeking experts in A.I. or machine learning.

The technology could help Disney tame soaring production budgets for its movies, an unnamed company executive told Reuters, as well as create new attractions for its theme parks.

But getting talent on board may be challenging. Musicians, including Drake (whose voice was mimicked on an unlicensed hit single in April), have complained that generative A.I. could deprive them of pay and undercut their own work. And among the demands of the striking Hollywood writers’ and actors’ unions are guardrails that limit movie studios’ ability to use A.I. to replace humans.

Not all artists are against the adoption of A.I. The singer Grimes, who has said she’s open to licensing her voice for user-generated work, told Wired that there were potential benefits to such an arrangement.

Some executives think it’s possible to strike a balance. “With the right framework in place, A.I. will enable fans to pay their heroes the ultimate compliment through a new level of user-driven content,” Robert Kyncl, the C.E.O. of Warner Music (which is also reportedly in talks with Google), told investors yesterday.

But Kyncl added, “The thing that is important is that artists have a choice, because there are some that may not like it, and that’s totally fine.”

The legal fight against corporate diversity policies ramps up

Even before conservative activists scored a win when the Supreme Court struck down affirmative action at universities, they began taking on initiatives meant to increase diversity across corporate America.

These campaigners are arguing that policies aimed at improving diversity, equity and inclusion — known as D.E.I. — violate rules meant to protect against race and sex discrimination. And, according to The Wall Street Journal, they’re seeing results:

Comcast settled a case accusing it of illegally favoring minority-owned small-business customers with grants and marketing advice. Amazon has been sued in Texas over a program offering an extra $10,000 to Black- or Latino-owned delivery-service contractors. Starbucks directors and executives are being sued by a shareholder arguing they violated their duty to investors by supporting diversity policies. …

Companies say their initiatives fall within the law. Many say they remain committed to increasing the demographic diversity of their workforces and suppliers, citing business benefits and the hurdles some groups continue to face in American corporations. Privately, many are asking their lawyers if and how much they should modify their methods in light of the affirmative-action decision.

THE SPEED READ

Deals

Abu Dhabi’s state-owned oil company, Adnoc, has reportedly assembled a team to invest $50 billion in deals to diversify its business. (FT)

The chairman of L’Occitane is said to be in talks to take the skin-care company private at a valuation of about $6.5 billion. (Bloomberg)

David Kurtz, the former head of Lazard’s restructuring practice who has worked on some of the biggest corporate bankruptcies, has joined the financial advisory firm Hilco. (Reuters)

Policy

The Supreme Court temporarily revived the Biden administration’s regulations for so-called ghost guns, which are built from kits ordered online and are largely untraceable. (NYT)

The Italian government partially backtracked on its plans for a windfall tax on banks, after lenders’ stocks slid when the initial policy was announced. (FT)

Best of the rest

Some Hollywood productions are being allowed to continue, despite the writers’ and actors’ strikes — and it’s not always clear why. (NYT)

A 143-year-old portrait of an obscure government official has set off a turf war between the Treasury Department and the Office of the Comptroller of the Currency. (WSJ)

“Trying to Process Your Q3? Journal About It.” (NYT)

We’d like your feedback! Please email thoughts and suggestions to [email protected].

Andrew Ross Sorkin is a columnist and the founder and editor at large of DealBook. He is a co-anchor of CNBC’s “Squawk Box” and the author of “Too Big to Fail.” He is also a co-creator of the Showtime drama series “Billions.” More about Andrew Ross Sorkin

Ravi Mattu is the managing editor of DealBook, based in London. He joined The New York Times in 2022 from the Financial Times, where he held a number of senior roles in Hong Kong and London. More about Ravi Mattu

Sarah Kessler is a senior staff editor for DealBook and the author of “Gigged,” a book about workers in the gig economy. More about Sarah Kessler

Michael de la Merced joined The Times as a reporter in 2006, covering Wall Street and finance. Among his main coverage areas are mergers and acquisitions, bankruptcies and the private equity industry. More about Michael J. de la Merced

Ephrat Livni reports from Washington on the intersection of business and policy for DealBook. Previously, she was a senior reporter at Quartz, covering law and politics, and has practiced law in the public and private sectors. More about Ephrat Livni

Source: Read Full Article

-

U.S. Covid Test Positivity Rises Above 9%

-

NDTV defers annual meeting by a week amid Adani group’s takeover bid

-

Biden Pardons Convicts In Federal Offenses Of Marijuana Possession

-

India keen to expand footprint in oil-rich Siberia

-

Tesla Ban On Employees Wearing Union Shirts Unlawful, Labor Board Rules