“Numerology” tries to find reality within various measurements of economic and real estate trends.

Buzz: Mortgage rates are back above the inflation rate for the first time in nearly two years.

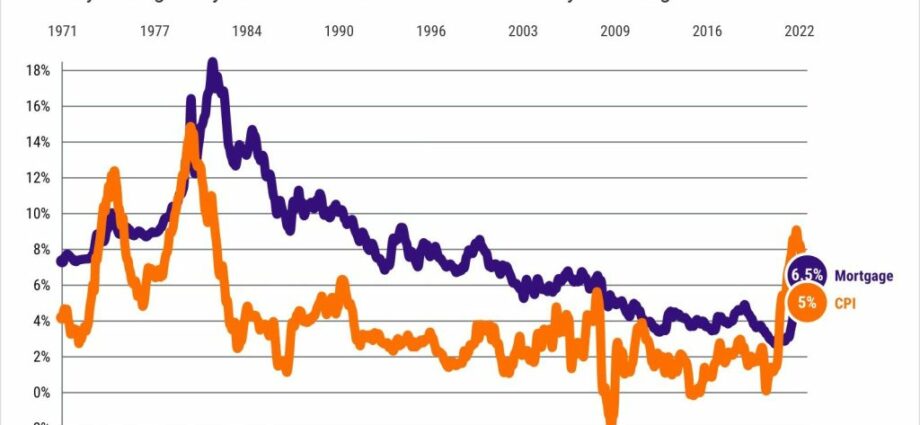

Source: My trusty spreadsheet compared Freddie Mac’s average 30-year month rates vs. the 12-month change in the Consumer Price Index as a way to gauge where this important loan rate should be.

Fuzzy math: What’s the proper level for mortgage rates without the Federal Reserve’s meddling?

Topline

Mortgage rates in March averaged 6.5% vs. a 5% inflation rate. That put home loans 1.5 percentage points above the rise in the cost of inflation. That’s the largest premium for home loans since November 2020.

Home loans priced above the inflation rate make economic sense. Lenders don’t want to be paid back with dollars deflated by a surging cost of living.

But during the pandemic era, the Federal Reserve used its powers to create historically cheap money as a boost to a coronavirus-chilled economy. Remember the 2.7% mortgages of late 2020?

That stimulus – plus other government aid – overheated the economy. It ignited the cost of living and ballooned home prices. Inflation hit 8.9% in June 2022.

That caused the Fed to morph from facilitator to party pooper, upping numerous interest rates to ice the economy.

Details

How generous was the Fed in the pandemic era?

Consider that in the 612 months of mortgage data tracked by Freddie Mac since 1972, home loans have been cheaper than inflation just 55 times – or 9%. And 22 of those oddities occurred in an unprecedented 22-month-run that ended in January.

In this recent period of gift-giving by the central bank — April 2021 through January 2023 — mortgages averaged 4.4% while inflation ran 6.9%, a stunning 2.5-point discount.

The only other time anything like this occurred was the 20-month streak that ended in July 1975. That era’s economic turmoil, highlighted by an Arab oil embargo, had mortgage rates averaging 9.1% vs. 10.6% inflation – and that was only a 1.5-point discount.

Ponder what history tells us about the premium that mortgage rates usually run ABOVE inflation …

The 1970s*: 8.9% mortgages vs. 7.3% inflation – 1.6-point premium. Slow-growth “stagflation” throttled the U.S. economy. (*Data starts in 1971.)

The 1980s: 12.7% mortgages vs. 5.6% inflation – 7.1-point premium. The Fed choked off inflation with pumped-up interest rates.

The 1990s: 8.1% mortgages vs. 3% inflation – 5.1-point premium. Borrowers suffered after the mortgage-making savings and loans collapsed.

The 2000s: 6.3% mortgages vs. 2.6% inflation – 3.7-point premium. Lenders were more focused on volume, not loan quality. Bad idea!

The 2010s: 4.1% mortgages vs. 1.8% inflation – 2.3-point premium. A return to conservative lending after the bubble burst into the Great Recession.

Bottom line

So what should 2023’s mortgage rates be if the economy is returning to a post-pandemic normal with inflation slowly retreating to near the Fed’s 2% targets?

Let’s take the 2010s as representative of the modern mortgage market. Its average 2.3-point premium would translate March’s 5% inflation rate to a 7.3% loan rate. So March’s 6.5% average 30-year rate seems like a bargain.

And current rates also seem like a good deal when pondering what mortgage rates have previously been when U.S. inflation was exactly 5% like it was in March.

In December 1976, 5% inflation came with 8.8% mortgages. October 1982 was at 14.6%, April 1989 at 11.1%, May 1991 at 9.5%, and September 2008 at 6%.

And here’s 52 years of history: Mortgage rates average 7.8% vs. 4% inflation.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at [email protected]

Source: Read Full Article

-

China’s Economy Faces Yet Another Threat: Falling Prices

-

Academy Museum Of Motion Pictures Voluntarily Recognizes Union To Represent Its Workers

-

European Shares Set To Rally On US Debt Deal

-

SAP Stock Down On Weak Q4 Profit, Sees Growth In FY23; To Cut 2.5% Jobs; Mulls Qualtrics Stake Sale

-

After Dish Network Beats Q4 Earnings Estimate, Chairman Charlie Ergen Pronounces Last Rites For Rising Carriage Fees: “The Next Step In Retrans Is Down, Not Up”