The low-fee private schools outperforming their expensive rivals in the HSC 2023-12-21 On: 2023-12-21

Major Crypto Exchange Drops Shiba Inu, Dogecoin, and Cardano in Canada Amid Delisting Wave, Stands by XRP 2023-12-21 On: 2023-12-21

XRP Lawsuit Update: Will the SEC Pay Any Reimbursement for Losing Against Ripple? – Coinpedia Fintech News 2023-12-21 On: 2023-12-21

Crypto Trader Turns $454 into $2.19 Million Trading Avalanche-Based Memecoin 2023-12-21 On: 2023-12-21

Solana Surge Prompts FTX's Comeback as Claim Prices Surge – Coinpedia Fintech News 2023-12-20 On: 2023-12-20

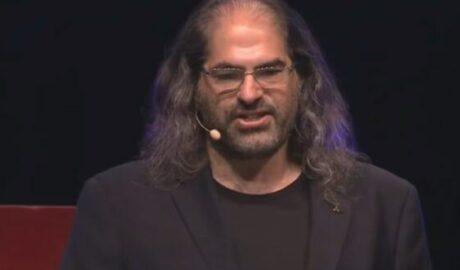

Driving Bitcoin's Surge: MicroStrategy Founder on Education, Adoption, and Policy Impact 2023-12-20 On: 2023-12-20

UK Payments Regulator Proposes To Cap Cross-border Fees On Mastercard, Visa Cards 2023-12-20 On: 2023-12-20

Judge Approves CFTC’s Record $2.7 Billion Settlement With Binance; Zhao To Pay $150 Million Fine 2023-12-20 On: 2023-12-20

'Kaboom Moment': Market Pundit Makes Strong Case For Ripple's XRP Rocketing Past $18 Price 2023-12-19 On: 2023-12-19

Terra-Luna Founder Do Kwon Wins Bid To Stop Extradition From Montenegro — For Now 2023-12-19 On: 2023-12-19

Colin Armstrong's daughter makes emotional plea for millionaire dad, 78, snatched in Ecuador…as son flies out for hunt | The Sun 2023-12-19 On: 2023-12-19